Governor Brian Kemp has amended the call for the June 2026 special session to allow consideration of local legislation necessary to implement the Local Homestead Option Sales Tax (LHOST) authorized by SB 33.

This action may accelerate local discussions regarding both LHOST and the Flexible Local Option Sales Tax (FLOST), and city officials may begin hearing from county officials or members of their local legislative delegation in the coming weeks.

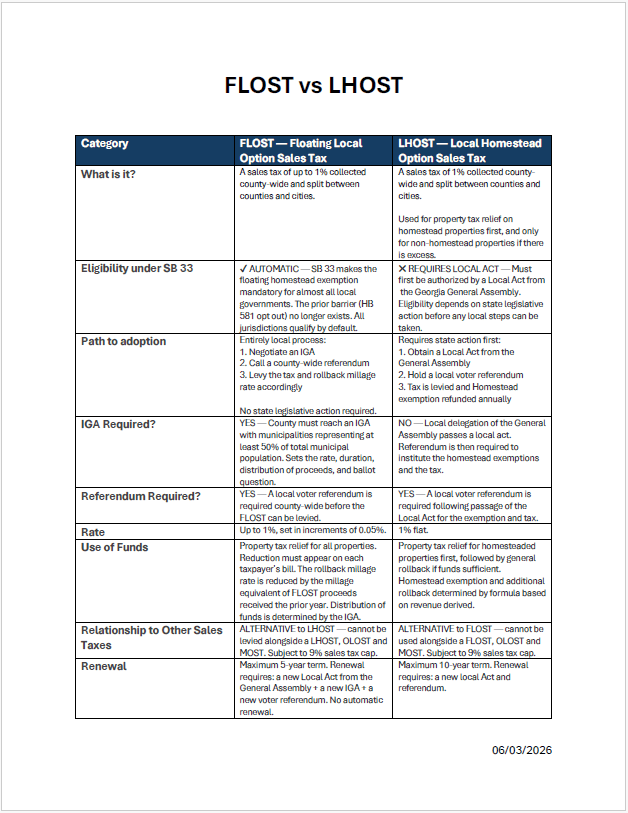

LHOST and FLOST both provide a mechanism to reduce property taxes through the use of local sales tax revenue. However, the two options differ significantly in how they are implemented.

LHOST requires local legislation for both the county and each municipality to participate. If approved by the General Assembly during the special session, the local legislation would place a referendum on the November 2026 ballot. If approved by voters, the sales tax would begin being collected on January 1, 2028, and the resulting property tax relief would not appear on city and county tax bills until fall 2028.

FLOST, by contrast, does not require local legislation. Instead, it may be called by agreement of the county and cities representing a majority of the municipal population within the county. Like LHOST, FLOST requires voter approval through a referendum. The sales tax then begins being collected at the start of the next calendar quarter and tax relief appears on the next issued tax bill.

Counties that are FLOST-eligible today because the county and all municipalities stayed under HB 581 could theoretically pursue a FLOST referendum in November 2026 if the required local agreement can be reached. Because SB 33 brings all cities and counties under HB 581 beginning in January 2027, all counties will also become eligible to pursue a FLOST referendum beginning that year, subject to local agreement and voter approval.

While both sales taxes are designed to provide property tax relief, they differ in the distribution and manner that relief is provided. LHOST funds are distributed by a formula exempting an equal amount of value from only homesteaded properties. FLOST funds by contrast are distributed between the county and cities based upon the agreement and are used to provide millage rate reduction for all property.

GMA's one-page summary outlines the key distinctions between LHOST and FLOST. A discussion of these issues will take place during the 2026 Annual Convention in Savannah.

City officials should carefully evaluate the potential impact of any proposal on their local tax structure, including assessed valuation growth, millage rates, existing sales tax revenues, and long-term fiscal stability. The financial effects of adopting LHOST, adopting FLOST, or maintaining the current structure may vary significantly from one community to another.

If your city is approached by county officials or members of the local legislative delegation regarding LHOST legislation during the 2026 special session, please reach out to Ryan Bowersox. While GMA does not advocate for or against local legislation, GMA staff can provide technical guidance and help cities understand the decision-making process, implementation requirements, and policy considerations associated with these proposals.